HOUSE PRICES TO FALL ?

September 14th 2020

The Centre for Economics and Business Research has forecast a 14% drop in house prices by the end of 2021.

Despite average prices reaching record highs in August, CEBR's analysis suggests that prices will start to fall significantly towards the end of the year and the first half of 2021, aside from a short spike as the stamp duty reduction comes to an end.

CEBR predicts that average house prices will be 13.8% lower in 2021 than in 2020.

CEBR says the housing market "defied gravity" in August, citing July's stamp duty cut as a main factor, which it predicts will spark a 1.2% increase in average prices and a 6.0% rise in the number of transactions "compared with what otherwise might have happened".

The Centre believes that the temporary nature of the tax reduction means that the policy’s short term effects could be even more dramatic, as people rush to complete transactions before the return to the previous stamp duty regime at the end of March 2021.

It also believes that pent-up demand during lockdown has sustained house prices. An estimated 150,000 house purchases that would otherwise have taken place were put on hold between March and June as a result of the coronavirus pandemic. Data from RICS suggests that buyers have returned to the market more quickly than sellers, boosting prices. Additionally, CEBR says the impact of the lockdown on low-income workers means that recent house price data is likely to have been skewed towards higher value properties.

CEBR also believes that the suspension of forced sales and repossessions will have had some supply side impacts on the overall housing market throughout the second and third quarters, boosting prices as well.

CEBR concluded: "What most of these factors have in common is that they are transitory in nature. Indeed, the Coronavirus Job Retention Scheme was cut after August and it, as well as the ban on mortgage possessions, is scheduled to end on 31st October, while stamp duty will revert to its original level in April 2021. Moreover, pent-up demand from the period of lockdown will eventually work its way out of the system in the coming weeks."

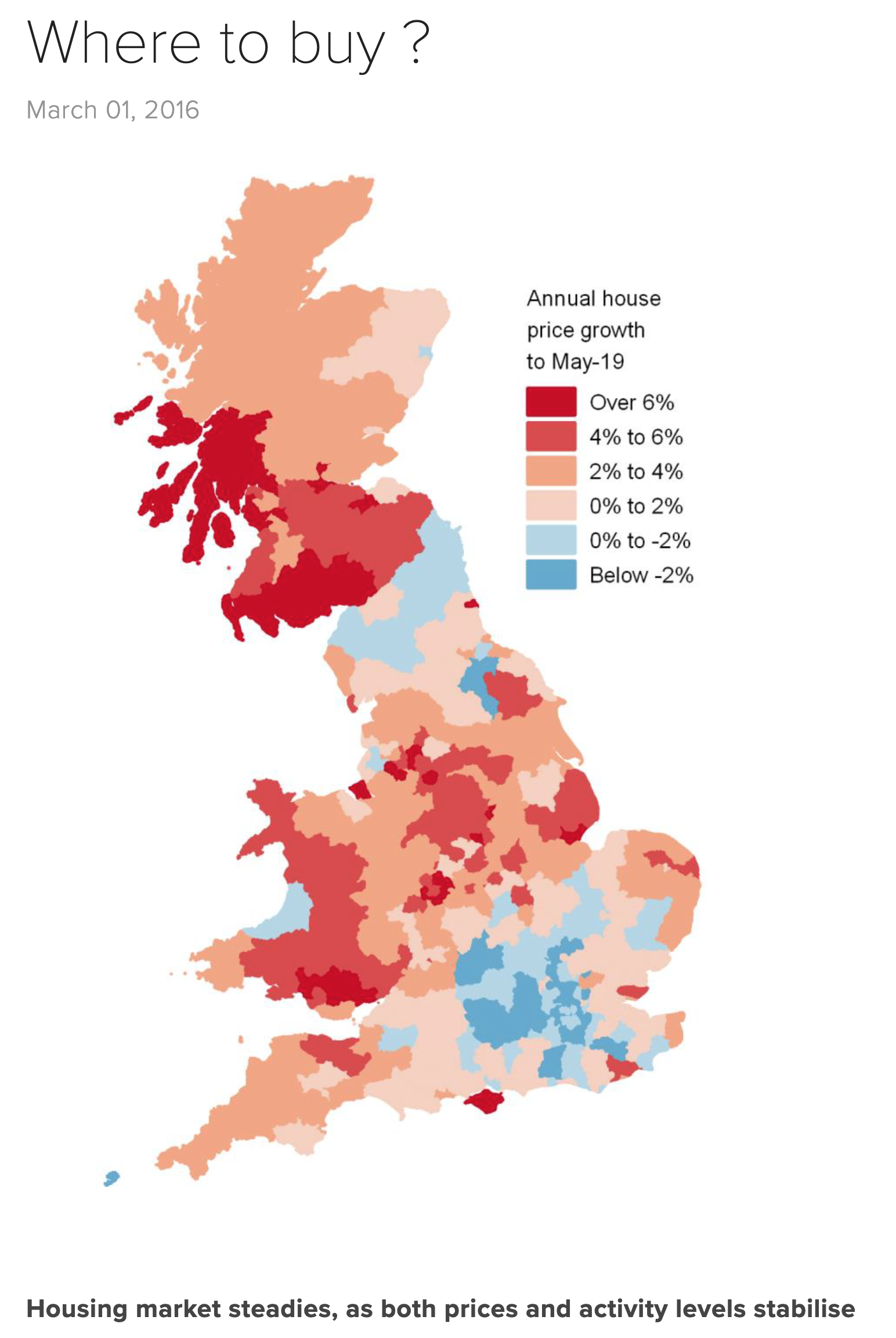

Where to buy ?

August 12, 2019

So here is the latest UK-wide graphic for the year May 2018-2019 house price courtesy of Savills.

Housing market steadies, as both prices and activity levels stabilise

House prices rose 0.3% in July, according to Nationwide, leaving annual growth also at 0.3%. This broadly flat national average hides the regional variation, with strong growth in the Midlands and Wales balancing out the falls in London and the South. It now looks likely that the UK will see zero average house price growth in 2019, undershooting the 1.5% growth we forecast last October, which assumed an orderly Brexit in March as per major economic projections at the time.

This zero price growth matches the latest RICS survey results, which saw roughly even numbers of surveyors reporting prices rising as falling. But there are greater signs of optimism, pointing to stabilising market values and volumes. More surveyors are now reporting price rises than at any time since August 2018. They are also showing increasing optimism in activity levels, with a narrow majority seeing rising numbers of both inquiries and instructions for the first time since last summer. This is supported by Land Registry transaction figures, which, while still declining, have been falling at a reduced rate over the past few months.

This modest strengthening in activity suggests some buyers and sellers gave up waiting for Brexit, following agreement of the current extension in April. Many buyers simply cannot delay moving indefinitely but will attempt to avoid peaks of uncertainty. The next is obviously the October Brexit deadline, when it is far from clear what will happen: Brexit with a deal, without a deal or a further extension. What actually happens will determine the speed and strength of any boost to activity levels. But as long as any lack of demand is matched by low numbers of people wanting to sell, prices are unlikely to see a major change.

Annual house price growth was the strongest in Blaenau Gwent at 17.4%, followed by Torfaen and West Dunbartonshire at 12.7% and 10.7% respectively. The largest falls were in Ealing of 6.5%, and in Tower Hamlets and Watford, both falling 5.8%.

National annual rental growth was 1.2% in the year to June. That rate of growth has been increasing since the start of the year. This may be driven by stronger wage growth over recent months and tenant demand, which has continued to grow according to the RICS survey, while landlord instructions to let have been falling. Assuming the wage growth trajectory is not deflected by Brexit, we would expect this mismatch between supply and demand to continue pushing up the rate of rental growth.